BLUF:

Walmart / Humana makes lots of sense. Most commentary misses the real opportunity though. In the short run this is growing Risk Adjustment reimbursement through improved diagnosis capture in retail clinics ($100s of millions in incremental profit). In the long run, this is about including social interventions (e.g. nutrition, fitness) as a part of health care and using that as a means of reducing cost and improving outcomes.Recently, talks of a Walmart / Humana partnership have been in the news. Most articles discuss expanding the delivery of traditional healthcare services in stores, which gives Humana beneficiaries access to cheaper and more convenient primary and urgent care. And Walmart hypothetically gets more people in stores, and more often, which could boost same store sales [1]. Humana saves money, Walmart gets a revenue boost.

I think these benefits, though, are quite marginal. This assessment completely misses the opportunities that are actually meaningful in a tie up.

One of these is a massive boost in Risk Adjustment-related reimbursement for Humana’s three million Medicare Advantage beneficiaries -- which could be worth $100s of millions in additional profit in a 2-3 year time horizon.

The other is the chance to totally refactor health care delivery in America in a way that marries existing medical interventions with social interventions. Humana could create models of care that harness not just physicians and hospitals, but physicians, hospitals, and any combination of stuff and space and services delivered through Walmart stores and supply chains. It would take real vision, patience, and strategic investment to get right. But the potential savings and improvement in health outcomes could be substantial.

I will start with a bit of context about the two companies, focusing mainly on the details that are pertinent here, then get into how the partnership could take shape.

What do I need to know about Humana?

Humana is one of the biggest health insurance companies in the United States. They brought in close to $54B revenue in 2017. They are relatively profitable for the industry, margin close to 5%. |

| Income statement from Humana's 2017 annual report [2]. |

The important thing to realize beyond this for our purposes is that the lion's share of Humana's revenue comes from Medicare Advantage (MA) - close to two thirds. It's also their main source of profit.

|

| Details from Humana's 2017 annual report. I circled the relevant bits showing our MA enrollment and revenue figures [2]. |

For the rest of this to make sense it is important to have some handle on what MA is and what Risk Adjustment (RA) is. Read the first three sections of my previous post on RA policy if this is unfamiliar to you.

What do I need to know about Walmart?

You know who Walmart is. You may not truly appreciate their scale, however, and some aspects of their business:- Probably more than one third of Americans walk through the doors of a Walmart each week and buy something [3].

- Conjecture, but I think that Walmart shoppers skew older, and an even higher percentage of Medicare Advantage beneficiaries shop at Walmart each week. I would bet it's more than half, perhaps substantially more.

- Walmart is already operating a number of retail clinics - some focused on primary care / immunizations, some on vision. Unclear exactly how many there are now.

- Walmart is the biggest grocer in America by a long shot. They are responsible for 15% of grocery sales in the country, twice as much as the next biggest player (Kroger) and more than an order of magnitude more than Whole Foods [4].

What can they do together, Part A: Risk Adjustment diagnosis capture

Recall that capture of diagnoses in medical claims drives Risk Adjustment payment for Medicare Advantage reimbursement. Recall that there are many individuals on Medicare Advantage plans who either never utilize care at all in a year and therefore do not have diagnoses recorded, or folks who utilize but for one reason or another reach the end of the year without having a diagnosis that contributes to RA payment coded in a claim.

Recall from the previous section that probably half of MA beneficiaries are going to Walmart each month (this involves some liberal assumptions but let's roll with it), and that many Walmarts host retail clinics and many more could.

There is a tremendous opportunity to improve diagnosis capture and drive Risk Adjustment-related reimbursement by funneling Humana MA beneficiaries to receive comprehensive exams in Walmart retail clinics. This alone is probably far more valuable than any savings Walmart could deliver by reducing cost of primary and urgent care, and far more valuable than any boost in sales that more foot traffic could bring.

Recall from the previous section that probably half of MA beneficiaries are going to Walmart each month (this involves some liberal assumptions but let's roll with it), and that many Walmarts host retail clinics and many more could.

There is a tremendous opportunity to improve diagnosis capture and drive Risk Adjustment-related reimbursement by funneling Humana MA beneficiaries to receive comprehensive exams in Walmart retail clinics. This alone is probably far more valuable than any savings Walmart could deliver by reducing cost of primary and urgent care, and far more valuable than any boost in sales that more foot traffic could bring.

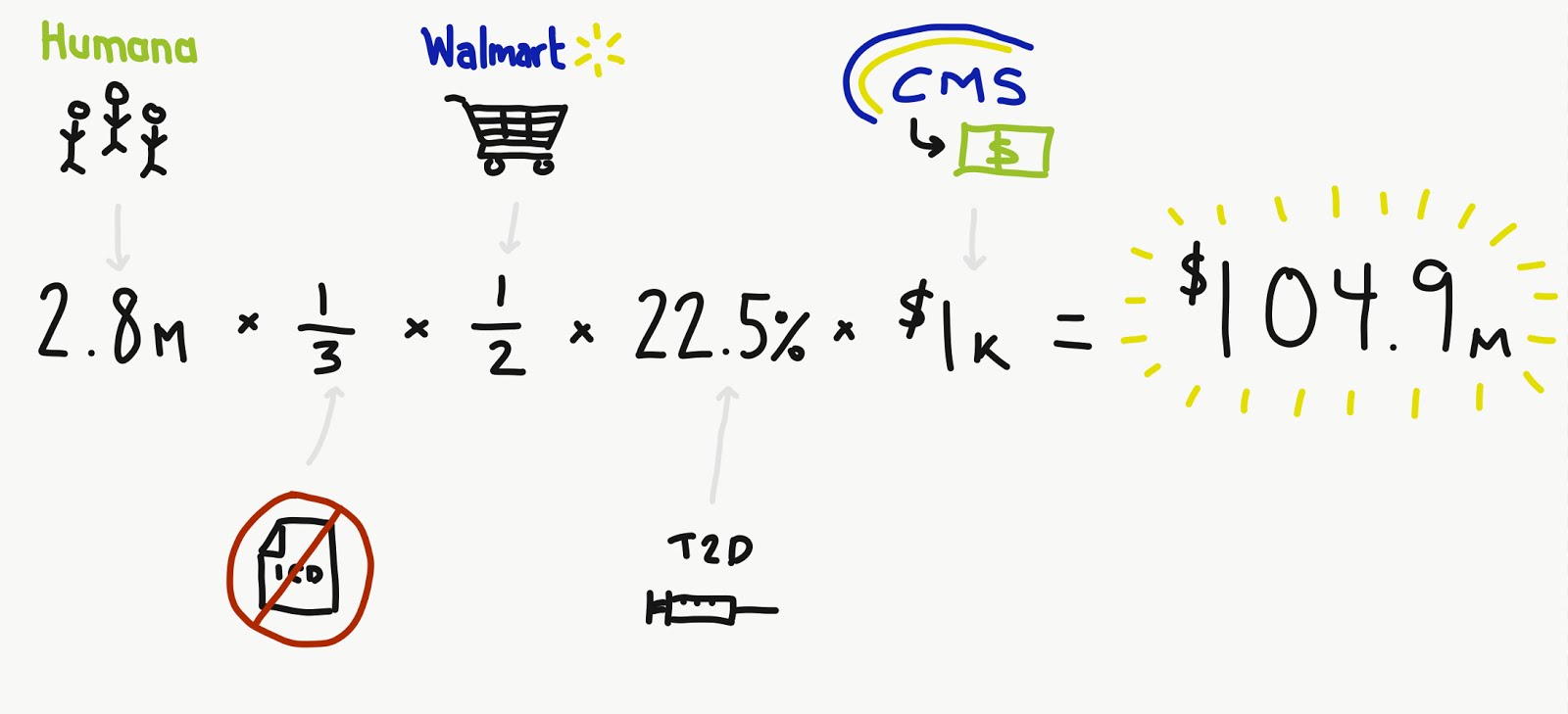

To give a sense of scale, let's walk through an exercise in estimating impact:

- Humana has a bit over 2.8 million individual MA members.

- Let's say about 1/3 of them don't have any claims at all in a given year.

- Let's say about 1/2 of those members without claims go to a Walmart at least once a month, and you can convince or incentivize them to visit a retail clinic in at least one of those visits.

- The population prevalence for diabetes in the US for adults >65 is 22.5% [5].

- The value of a recorded type 2 diabetes diagnosis is about $1,000 in annual revenue.

|

| The above calculation, visualized. It is important to note that there are a LOT of assumptions baked into this number but nothing here is completely unreasonable in the absence of additional information. You can play around with the parameters and regardless you will reach the same conclusion: this is a big opportunity. |

This would not necessarily do much for health outcomes. Open question as to whether these primary care visits result in any follow up, and if that follow up is medically useful.

What can they do together, Part B: the bigger project of health care delivery

Part B is the exciting part. It will take longer to see results here, but Part B represents the possibility of truly transforming health care delivery by harnessing Walmart's vast infrastructure.Consider that most health insurance companies have plenty of cash and a vested interest in your health but their ability to actually interact with you is quite limited. They can send you letters and they can pay your claims when you go to the doctor. But if you think about it, many of the key determinants of health may be things like food access, ensuring folks don't skip prescriptions, and (particularly in the elderly Medicare Advantage population) fitness and physical activity to keep bodies strong to avoid injury, e.g. hip fracture. But it isn't so easy to pay for your grocery bill in the current universe. And I don't think Blue Cross covers Zumba. But maybe it should or it is at least an experiment worth running.

An insurer partnering with Walmart suddenly gains access to stores full of groceries, equipment, space for activities, and consistent non-hospital face time with members. It is a chance for Humana to pay for something other than doctors to improve your health. It's hard to say a priori what exact interventions will be impactful. But given Walmart's scale and Humana's beneficiary count, you can begin to run tens if not hundreds of small pilots and then scale up what is working and refactor or discontinue what is not.

Some limited work has been done on quantifying the impact of lifestyle interventions: one recent success story however is Geisinger's work in "prescribing" food to members with uncontrolled diabetes. Focusing on food and counseling versus simply paying for medical bills resulted in an astonishing $8,000 per member per month savings and a two point average drop in hemoglobin A1c levels, a key marker of diabetes severity. This is a big deal. Walmart / Humana working together could probably replicate and scale this up for the populations they serve -- Humana folks get pre-selected bags of groceries for free each week when they visit Walmart [6].

But Walmart stores provide a combination of physical stuff and physical space to try just about anything. Maybe it's just space for senior-center type activities.

I do not think there would be any quick wins here. This would take vision, investment, and lots of failures before honing in on what actually keeps beneficiaries out of the hospital. But the end result could be a Humana that outperforms all other payers and the integrated payer providers (e.g. Kaiser, Intermountain, Geisinger): much better health, at a much better price.

|

| Walmart partnership opens up new ways for a payer to interact with its membership base, beyond emails, phone calls, and paying bills for providers. It's very hard to say how this will evolve. The most valuable way the stores could be used will probably have to be discovered through experimentation and does not resemble anything above. But I suspect there is something here. |

Other thoughts?

There could be (and probably is) a whole drug buying and distribution story that I am completely missing here. Not something I understand well enough.Parting thought: if a project with Humana works well, nothing stops Walmart from scaling its healthcare practice out to the rest of the country, possibly with other payers. Walmart has a physical presence and supply chain everywhere. If I am a hospital system, I am watching this closely. If I am a payer I probably am too.

References:

[1] https://www.nytimes.com/2018/03/30/business/walmart-humana-merger.html[2] https://humana.gcs-web.com/static-files/c7a3ff1d-4a42-44b1-9284-342d4997366f

[3] https://blog.walmart.com/business/20161003/the-grocery-list-why-140-million-americans-choose-walmart

[4] https://www.cnbc.com/2017/06/21/dont-worry-wal-mart-amazon-buying-whole-foods-is-just-a-drop-in-the-bucket.html

[5] https://www.cdc.gov/diabetes/pdfs/data/statistics/national-diabetes-statistics-report.pdf

[6] https://hbr.org/2017/10/how-geisinger-treats-diabetes-by-giving-away-free-healthy-food

No comments:

Post a Comment