BLUF:

I previously proposed some changes to Risk Adjustment in Medicare Advantage / Marketplace that would reduce unnecessary administrative expenditure on home health visits. I got feedback from stakeholders in industry and academia: largely positive, but some critical. Below I present the feedback, changes to consider in light of that feedback, and propose concrete analyses that could validate the proposal.By way of quick recap, in a previous post I identified unnecessary administrative expense in Medicare Advantage (MA) and Marketplace plans related to Risk Adjustment (RA). In pursuit of Hierarchical Clustering Code (HCC) capture geared at higher reimbursement levels, insurers are incentivized to send for home health visits to code diagnoses as an administrative exercise.

|

| A valuable proposition. |

One other thing to consider: this in some sense levels the playing field across payers. You are competing more on your ability to provide good, low cost care, rather than winning the HCC game, which could tilt things in favor of the payers most willing to invest in gaming the system.

Another thing to consider: this may lower the barrier to entry for new MA plans or Marketplace plans, given that your RA related payments will be more predictable and smooth. You don't have to go through the exercise of setting up assessment infrastructure. You need to worry less, in the Marketplace case, about what your peers are up to with respect to home health exams -- it stops a putative arms race. This is speculative though.

And so without further delay - here are some points folks made in an initial round of feedback gathering, and my responses.

1. What diagnoses would you consider chronic and count for multiple years?

This is challenging because there are some diagnoses that never go away - severe, genetic diseases like hemophilia; amputations; etc. Then there are is another tier of diseases that tend not to go away like COPD, CHF, autoimmune disease, etc. Then there are diseases that occur once and are probably cured like a bacterial infection.

This would require medical expertise to get right but broadly, a way to approach this might be to consider diagnoses in these three tiers and treat them differently accordingly. For example (don't pay too much attention to the names of the categories):

- Tier 1 - Persistent Disease:

- These never go away with time (e.g. genetic disease).

- Encountering the ICD once ensures that the HCC is perpetually assigned. For example if we get a claim for HCC066 Hemophilia (worth about 40) in 2014 and only 2014:

- 2015 reimbursement: worth 40

- 2016 reimbursement: worth 40

- 2017 reimbursement: worth 40

- Tier 2 - Chronic Disease:

- These tend not to go away with time / resolution is uncommon.

- Encountering the ICD in on year carriers over to multiple years as an HCC, however in the years after the initial diagnosis we apply a decay factor, say we are looking at HCC048 Inflammatory Bowel Disease (worth 1.70). We see the diagnosis in 2014 and only 2014:

- 2015 reimbursement: worth 1.70

- 2016 reimbursement: worth 1.70*(0.5)^1 = 0.85

- 2017 reimbursement: worth 1.70*(0.5)^2 = 0.425

- If we were to see the disease again in 2016 on a claim, it would "reset" the decay clock for 2017 reimbursement and look like:

- 2015 reimbursement: worth 1.70

- 2016 reimbursement: worth 1.70*(0.5)^1 = 0.85

- 2017 reimbursement: worth 1.70

- Tier 3 - Acute Disease:

- These are quickly resolved or must be actively treated.

- Encountering the ICD counts only within the given year. For example if you are assigned HCC131 Acute Myocardial Infarction (worth 8.6) in 2014 and only 2014:

- 2015 reimbursement: worth 8.6

- 2016 reimbursement: worth 0

- 2017 reimbursement: worth 0

Tier 2 is nice because you bias towards persistence, but you allow the diagnoses to decay away if the condition appears to be resolving itself.

Again, you need medical expertise to get this right. Probably whichever body came up with the HCCs to begin with should weigh in here.

2. This is going to significantly raise average scores / HCC prevalence. How should we address that?

Obviously there will need to be some re-calculation of multipliers - will need to downwardly adjust many HCC factors, since I suspect many more folks will wind up with an assignment for diabetes, COPD, etc.

In ideal world, whatever money you are losing in factor magnitude you should be regaining through increased prevalence; average beneficiary risk score should stay constant, e.g in a set of 8 beneficiaries, 4 people have a disease and 2 have it coded appropriately:

- Old: [1, 1, 1, 1, 1, 1, 2, 2] average = 1.25

- New: [1, 1, 1, 1, 1.5, 1.5, 1.5, 1.5] average = 1.25

A good way to calibrate would be to run the new methodology over previous years and make sure you are within a certain percentage range of the actual in-year reimbursement.

3. What about misdiagnosis? This is a bigger problem if HCCs stick year over year.

This is true - one trip to the ER where a sprain is misdiagnosed as gout could result in many years of inappropriately high reimbursement. I think there are three ways that we can think about addressing this:- Decaying HCC values (see first question above). I figure that if a diagnosis is incorrect, then it will quickly be extinguished by decay - and those who truly have the disease will see the full weight of the HCC factor persist because the ICD will recur year over year.

- Some clinical environments are more trustworthy than others: I'd tend to place less weight on an emergency room or urgent care setting. Maybe we simply should not consider ER or urgent care diagnoses in HCC assignment.

- Just don't worry about it and down adjust reimbursement. You would worry about misdiagnosis more if there was disparate impact across health plans. But there probably would not be. And so if everyone is hit with the same burden of inappropriate HCCs, does it matter?

4. Why hasn't this been done already?

Good question. This is not the first time this issue has been identified: https://www.publicintegrity.org/2014/06/10/14880/home-where-money-medicare-advantage-plansThe whole problem here is quite nuanced and evades quick description. I think the complexity of the failure makes it harder to sell. But this is just conjecture.

Where should we go from here?

I think there are a couple of analyses that need to be conducted as follow ups:

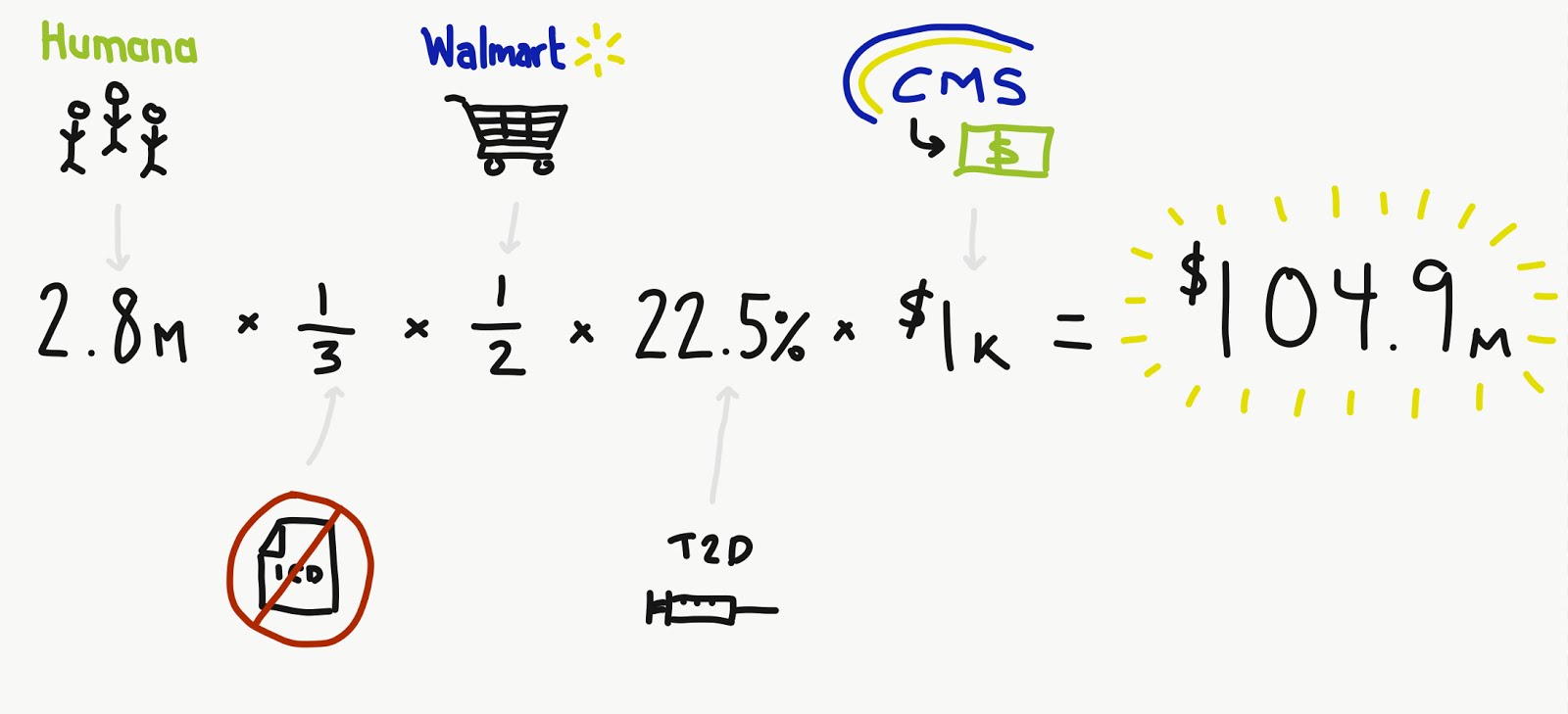

- Size of impact: this began with the premise that RA-related home health visits represent unnecessary administrative expense. There is cost and inertia to over come in making any policy changes. What is the amount of waste here? How much is this costing the American public?

- Medical utility: If these home visits are actually useful to beneficiaries commensurate with their cost then perhaps the change is worth reconsidering. My hypothesis is that they are not. This will actually be difficult to assess without a randomized, controlled trial.

- Simulating a new model: As mentioned earlier, this new model should result in roughly similar average beneficiary risk score and so we would want to:

- Tier diagnoses;

- Assign new weights;

- Simulate scores for a variety of plans operating in a variety of geographies and ensure that there are no big swings.

All of these could be done with MA claims from CMS.

If they could be answered in sequence, then I would have reasonable confidence that this is a change worth making.